| 17 | Differential accumulation |

| Past and future |

… he began to decipher the instant that he was living, deciphering it as he lived it, prophesying himself in the act of deciphering the last page of the parchments, as if he were looking into a speaking mirror. Then he skipped again to anticipate the predictions and ascertain the date and circumstances of his death. Before reaching the final line, however, he had already understood that he would never leave that room, for … everything written on them was unrepeatable since time immemorial. . . .

—Gabriel García Márquez, One Hundred Years of Solitude

Like other aspects of the capitalist nomos, there is nothing ‘natural’ about differential accumulation. To accumulate differentially is to creorder organized power — and to do so conflictually against multiple oppositions. Such a process cannot be predetermined. It has neither a preset pattern, nor an inevitable outcome. In fact, it doesn’t even have to happen and can just as easily go into reverse.

Given this open-endedness, the stylized history of differential accumulation is nothing short of astounding. With only brief interruptions, US-based dominant capital has managed to sustain its differential accumulation through both ‘prosperity’ and ‘crisis’ — and to do so in a most counterintuitive fashion. Its differential expansion has tended to rely not on green-field growth and cost cutting as the canons would have preferred, but on mergers and acquisitions and stagflation. Moreover, as we shall see in this final chapter, the broad trajectories of amalgamation and stagflation have become so tightly correlated that they look like mirror images of each other: as one process increases the other tends to decrease, and vice versa.

The apparent automaticity of the process may give the impression of natural inevitability, but that would be the wrong conclusion to draw. Perhaps a better metaphor here is the evolution of an organized religion. Much like the almighty God invented by past rulers, the ideology and practice of differential accumulation were created by capitalists as an open-ended process to increase their power. But success brings consolidation, and as dominant capital triumphed, its differential accumulation petrified into a rigid structure: it ended up conditioning and subjugating not only the underlying population, but also its own creators.

In the pages that follow we focus on one key aspect of this structure: the meta-correlation between amalgamation and stagflation. The historical relationship between these two regimes provides a framework for understanding key moments in the twentieth-century evolution of capitalism, as well as the limits it may face in the future.

Amalgamation versus stagflation

Figure 17.1 contrasts the general contours of internal breadth and external depth in the United States. The chart plots our amalgamation index (the buy-to-build indicator) against a composite stagflation proxy, both smoothed for easier comparison.

Figure 17.1: Amalgamation and stagflation in the United States

* Computed as the average of: (1) the standardized deviations from the average rate of unemployment; and (2) the standardized deviation from the average rate of inflation of the GDP implicit price deflator.

** Mergers and acquisitions expressed as a per cent of gross fixed private domestic investment.

Note: Series are shown as 5-year moving averages (the first four observations in each series cover data to that point only).

Source: The stagflation index is computed based on data from the U.S. Department of Commerce through Global Insight (series codes: RUC for the rate of unemployment since 1929; PDIGDP for the GDP implicit price deflator); Historical Statistics of the United States (series D8, p. 126 for the rate of unemployment before 1929). For the Amalgamation Index see Appendix to Chapter 15.

To clarify the meaning of our stagflation proxy, recall from Chapter 16 the weak definition of stagflation as inflation together with unemployment and underutilized capacity. Now, as we have seen, the United States experienced some measure of unemployment and under-capacity utilization throughout the past century, so in that sense there was always some degree of stagnation. Also, with the exception of the 1930s, there was uninterrupted inflation. Applying both observations to the weak definition implies that US inflation during the period was always stagflationary.

With this understanding in mind, our stagflation proxy combines inflation and stagnation in three simple steps: first, we measure the standardized deviations of inflation from its average; second, we compute the standardized deviations of unemployment from its average; and finally we take the average of the two indices. Since the United States experienced continued stagflation, we treat a zero reading of the combined index as the average rate of stagflation; a positive reading as above-average stagflation; and a negative reading as below-average stagflation.

The chart shows that over the long haul mergers and acquisitions were indeed the path of least resistance (Proposition 2 in Chapter 14). Whereas stagflation moved sideways, oscillating around its own stable mean, mergers and acquisitions rose exponentially relative to green-field investment (note the logarithmic left scale).

The chart also shows that, following the initial emergence of big business at the turn of the twentieth century, internal breadth and external depth tended to move counter-cyclically. Temporary declines in mergers and acquisitions typically were ‘compensated’ for by sharp increases in stagflation; and when amalgamation resumed, with dominant capital breaking through its existing envelope and into a broader universe, stagflation promptly abated (Propositions 1 and 8).

The very existence of this counter-cyclical pattern is already remarkable — particularly since, as we have repeatedly emphasized, differential accumulation does not have to happen and can as easily go into reverse. Note also the highly significant fact that the inverse correlation between breadth and depth has grown tighter over time.

This tightening is clear from the chart. During the final decade of the nineteenth century, when big business was only starting to take its modern shape, the two series still moved in the same direction. By the first decades of the twentieth century, however, with dominant capital already having assumed centre stage, the relationship turned clearly negative, although still somewhat loose. And from the 1930s onward, as differential accumulation became increasingly entrenched, the negative fit grew tighter and tighter.294

The progressive move from looser to tighter correlation is consistent with our earlier narrative. Differential accumulation, understood as a broad historical process, is relatively new. It rose to prominence only toward the end of the nineteenth century, when corporations grew big enough and became sufficiently intertwined with governmental organs to engage in large-scale strategic sabotage. The process first became important in certain sectors in the United States and Europe, from where it subsequently spread domestically and internationally. However, the spread was very uneven; and so, despite high capital mobility, initially the cyclical regimes in different sectors and countries were disjoined and out of step with one another. It was only later — with the gradual proliferation and deepening of business principles and the ideology of discounting, with the progressive breaking of sectoral envelopes, and with the growing globalization of ownership — that differential accumulation became the compass of modern capitalism. And therefore it was only toward the middle of the twentieth century, when these processes converged, that breadth and depth grew more stylized and inversely synchronized.

The pattern of conflict

Now, since differential accumulation lies at the heart of the capitalist creorder, its specific regimes are important for understanding the broader nature of institutional and structural change in capitalist society.

Perhaps the most important change concerns the pattern of conflict. Recall that although dominant capital always struggles to increase its power relative to other capitalists, in breadth this struggle is direct, whereas in depth the path is indirect. When expanding through breadth, capitalists fight each other to control existing and new corporate organizations. The intra-capitalist struggle here is commonly associated with overall growth and ongoing institutional change, which in turn partly conceals the conflict between capitalists and society at large. By contrast, in depth the intra-capitalist struggle is mediated through a redistributional conflict between capitalists and the rest of society; moreover, the redistribution here thrives on stagflation, not growth. Obviously, sustaining such accumulation-through-crisis requires entrenchment, fortified power arrangements and a greater use of force and violence.

The very different social conditions required for each regime explain their incompatibility. Individual firms can engage in both breadth and depth; but for society as a whole, the power processes that support one type of differential accumulation tend to undermine the other.

A new type of cycle

Cyclical analyses of capitalism tend to focus on the patterns of ‘real economy’. The most famous is the ‘business cycle’, a relatively short oscillation that describes the ups and downs of ‘economic activity’ — from output and invest ment to inventories and employment. Long-wave cycles, often extending over decades, measure looser variables such as innovation, as well as nominal quantities like prices.

These analyses are all informed by the traditional bifurcation between economics and politics. Embedded in the material/economic sphere, they emphasize the ‘automatic’ underpinnings of the cycle and search for their mechanical rationale.

After the Great Depression and the rise of ‘government intervention’, the business cycle was augmented by political ‘variables’. Although economists continued to keep their economy conceptually separate from politics, they recognized that the latter could contaminate the former, leading to a ‘political business cycle’.295

Our own breadth and depth cycles present a different story altogether. First, they deal neither with ‘economic activity’ nor with ‘government intervention’ that supposedly ‘distorts’ or ‘supports’ such activity; instead their subject is the broad creording of capitalist power quantified through differential accumulation. Second, although the breadth and depth cycles are historically stylized and seemingly mean-reverting, there is nothing automatic or equilibrating about them. In fact, given that we deal here with open-ended conflict whose outcome is never predetermined, there is no inherent reason why amalgamation and stagflation should be cyclical in the first place; and certainly there is no reason for the two cycles to be related.

The fact that they are cyclical and that they are correlated attests to the extent to which differential accumulation has come to define the capitalist nomos. Our own thesis is that for differential accumulation to occur, dominant capital has to expand through either breadth or depth; and that, at the societal level, these two regimes, because of their very different if not opposite character, tend to move counter-cyclically. But the grip of dominant capital can loosen or disappear, and when it does — so will differential accumulation and its cycles of breadth and depth.

Oscillating regimes: a bird’s eye view

With this open-ended conflictual framework in mind, we can tentatively identify several broad phases in the global evolution of differential accumulation, temporal patterns whose initially blurred contours have gradually sharpened into focus: (1) a mixture of breadth and depth during the period between the 1890s and 1910s; (2) a partial breadth regime during the 1920s; (3) a depth regime in the 1930s; (4) a breadth regime between the 1940s and 1960s; (5) a return to depth in the 1970s and early 1980s; (6) the re-emergence of breadth in the late 1980s and 1990s; and (7) tentative signs of a return to depth in the early years of the twenty-first century. Let’s look at each period a bit more closely.

The period from the 1890s until the 1910s was one of rapid and accelerating economic growth, coupled with relatively low inflation and the beginning of corporate transnationalization, particularly by large US-based companies. Internationally, differential accumulation was still cloaked in ‘statist’ clothes, with American and European companies often seen as imperial agents as well as pursuers of their own interests. The competitive expansion of these companies, however, was largely uncoordinated and soon led to the creation of massive imbalances of excess capacity. Left unattended, such imbalances would have spelled business ruin, so there was growing pressure to ‘resolve’ the predicament via depth. And indeed, as Figure 17.1 shows, since the middle of the first decade of the twentieth century US merger activity had collapsed, followed in the 1910s by war in Europe together with plunging production and rising inflation around the world.

The 1920s offered a brief break. In the United States, merger activity soared while stagflation subsided sharply. In Europe, however, the reprieve was short and stress signs were soon piling up. Protectionist walls, both between and within countries, emerged everywhere; stagflation spread through a cascade of crises; and before long the world had fallen into the Great Depression of the 1930s.

By that time, the counter-cyclical pattern of breadth and depth became more apparent, with declining merger activity accompanied by rising stagflation.296 The new depth regime was marked by the massive use of military force, in which the global power impasse was ‘resolved’ through an all-encompassing world war. This use of violence was articulated and justified largely in statist terms: it was a war of sovereigns waged over territory and ideology. But the war also proved highly significant for differential accumulation. Most importantly, it accelerated the relative ascent of US-based corporations, and it helped spread both the normal rate of return and the need to beat it.

After the war, the world again shifted to breadth. The counter-cyclical regime pattern was sharpened even further, while the inverse correlation between inflation and growth became increasingly apparent. Now, on the surface, it looked as if developments during that period, which lasted until the end of the 1960s, should have undermined breadth. For one, superpower rivalry, decolonization and the non-alignment movement limited the geographical expansion of Western dominant capital. In addition, many developing countries that were previously open to foreign investment adopted import-substitution policies that favoured domestic over foreign capitalists.

And yet, for much of the 1950s and 1960s, these barriers on breadth were outweighed by two powerful counter-forces. The first of these was the postwar baby boom that boosted population growth. The second was the postwar rebuilding of Europe and Japan that in some sense was equivalent to the re-proletarianization of their societies. The result was a powerful breadth engine, particularly for the large US firms that saw their profit soar during that period. The macroeconomic result in the industrialized countries — anomalous from a conventional viewpoint but consistent with differential accumulation — was rapid economic growth averaging 6 per cent during that period, combined with low inflation of less than 3 per cent.297

This picture was inverted in the 1970s. By then, the German and Japanese miracles had already run out of steam, while Western rates of population growth dropped sharply. Foreign investment could have provided a way out, yet outlets for such investment in developing countries remained hindered by communist or import-substituting regimes. Faced with these obstacles to breadth, dominant capital groups in the industrialized countries were once again driven toward depth, with the average rate of inflation during the 1970s rising to 8 per cent and the average rate of economic growth dropping to 3 per cent. And, as before, the new depth regime was accompanied by heightened conflict and violence. This time, though, the conflict was played out mostly in the outlying areas of the developing world, initially in South East Asia and subsequently in the Middle East.

The role of the Middle East

The role of the Middle East in global capitalism provides a good illustration of the temporal spread and geographical integration of differential accumulation.298 Until the late 1940s, the region was ‘out of sync’ with the global cycle of breadth and depth. Its energy resources had already been parcelled out by the international oil companies in the 1920s; but with the world awash with oil, these companies mostly ‘sat on their concessions’ and produced little. As a result, the Middle East remained relatively insulated from the capitalist core, and when Europe slipped into stagflation and conflict during the 1920s and 1930s, the region prospered. After the war, though, the tables turned. The Middle East — until then a true ‘outlying area’ — suddenly became centre stage for the global drama of differential accumulation.

Initially, the link was pretty simple, with oil from the region helping sustain the growth underpinnings of global breadth. During the early 1970s, however, when differential accumulation shifted into depth, the relationship became more complicated. The background for this latter shift is illustrated in Figure 17.2. The chart shows a positive long-term correlation between inflation in the industrialized countries on the one hand and the global arms trade expressed as a share of world GDP on the other. Conventional economics would probably treat this relationship as accidental and largely irrelevant. From the viewpoint of dominant capital, however, the relationship is systematic and meaningful: it points to the conflictural underpinnings of its differential accumulation cycles.299

Figure 17.2: Inflation and arms exports

Note: Series are shown as 3-year moving averages.

Source: International Financial Statistics through Global Insight (series codes L64@C110 for CPI); U.S. Arms Control and Disarmament Agency, World Military Expenditures and Arms Transfers (various years).

As we noted earlier, the inflationary depth regime of the 1970s and 1980s was largely a response to Western dominant capital ‘running out of breadth’. This exhaustion in turn was partly the consequence of bipolar geopolitics that prevented capitalist expansion into outlying areas and contested Western control over strategic regions, particularly the Middle East. One key consequence of this antagonism was an intense arms race, and hence it is not surprising that the time pattern of arms exports — a handy proxy for ‘bellicosity’ — roughly follow the periodicity of Western inflation: the first process was fuelled by and nourished the antagonism and violence of depth, the second its redistributional mechanism. Both arms exports and inflation rose until the mid-1980s, peaked as the Cold War began to weaken, and went into a free fall with the disintegration of communism and the onset of global breadth.300 Moreover, the two processes were causally connected, with military conflict, especially in the Middle East, contributing to rising energy prices, and therefore to higher inflation.

The late 1980s seemed to mark the beginning of yet another breadth phase — this time at the global level. On the surface, the new breadth regime was somewhat anomalous according to our criteria: inflation in the industrial countries dropped sharply, and yet, unlike in previous cycles, growth did not revive. A closer inspection, however, easily shows why.

First, with the collapse of the Soviet Union and the wholesale capitulation of statist ideology, the entire world finally opened up for capitalist expansion and differential accumulation. The result was that, although external breadth for dominant capital fizzled in the industrial countries proper, it remained strong outside of these countries, particularly in developing Asia.301 Moreover, cheap imports from Asia helped keep inflation in the industrial countries low despite the latter’s domestic stagnation. Second, the ideological demise of public ownership and the ‘mixed economy’ opened the door for privatization of state assets and government services, which, from the viewpoint of dominant capital, was tantamount to green-field investment.302 And third, the decline of statist ideology weakened the support for ‘national’ ownership, thus contributing to the spread of cross-border mergers and acquisitions. Together, the combination of expansion into less developed countries, privatization and corporate amalgamation helped sustain a powerful breadth drive for large Western corporations despite the lacklustre growth of their ‘parent’ countries.

Coalitions

So far, we have focused on dominant capital as a whole. The concrete history of differential accumulation, however, including its transition from one regime to the next, depends crucially on what happens within dominant capital. This process includes the inner conflicts between various corporate-state coalitions and alliances that comprise the nuclei of dominant capital, as well as the struggles that pit these coalitions and alliances against groups outside of dominant capital. An analysis of these issues is beyond the scope of this volume, but their significance can be illustrated briefly.303

During the depth phase of the 1970s and 1980s, differential accumulation was led by a ‘Weapondollar–Petrodollar Coalition’ made up of large oil companies, armament contractors and OPEC, and was backed by the United States and several European governments that supplied arms to the Middle East and encouraged high oil prices.304 The central accumulation mechanism of this coalition was the ongoing cycle of Middle East ‘energy conflicts’ and ‘oil crises’. The basic logic of the process was simple enough. Rising petroleum prices brought massive profits for the oil companies. They also generated huge petrodollar revenues for local OPEC governments, who were only too eager to spend them on expensive weaponry in preparation for the next war. As a result, the Middle East during that period became the world’s largest market for imported arms, absorbing over one third of the global trade. The big arms contractors of course loved this arrangement, and various US administrations — from Nixon’s and Ford’s to Bush Sr.’s and Jr.’s — supported it with equal zeal. Indeed, what better way to fight communism, divide and rule the Middle East, and enrich your corporate friends — all in one stroke and without spending a penny?

The consequences of this process were nothing short of dramatic. Rising oil prices threw much of the world into a deep stagflationary crisis, conflict bloomed everywhere, and there was even the occasional flirt with nuclear exchange. The Weapondollar–Petrodollar Coalition, however, thrived, while the other members of dominant capital — although hit by the stagnation — ended up benefiting greatly from the consequent inflation (revisit Figure 16.3).

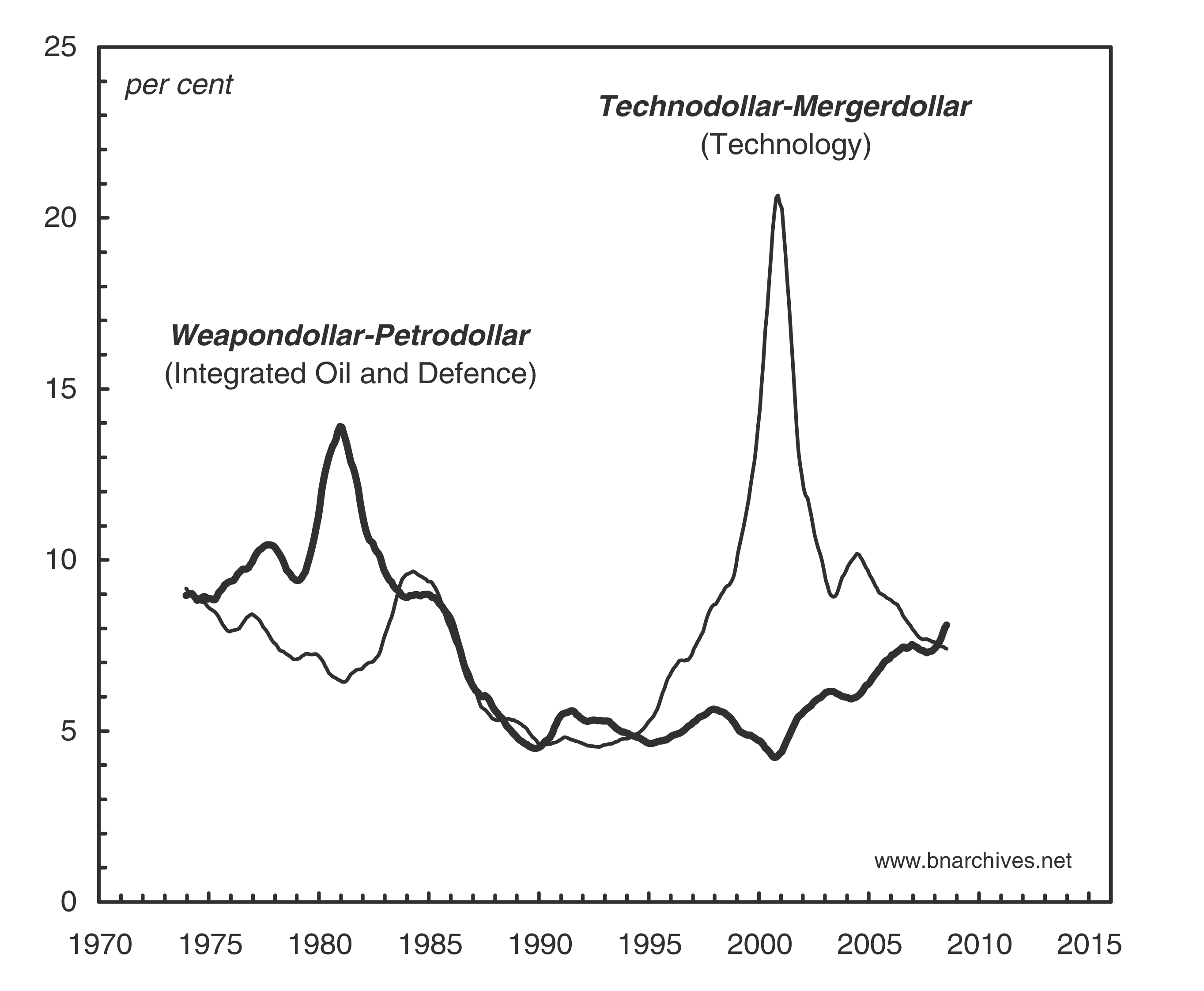

The distributional consequences for the oil and armament companies are vividly illustrated in Figure 17.3 which measures their share of global market capitalization. As the chart shows, during the 1970s and 1980s, this group of firms became one of the world’s most valuable. With plenty of wars and soaring oil prices, its fortunes multiplied; and by 1981, after the onset of the Iran–Iraq wars, it accounted for nearly 14 per cent of global market capitalization. ‘War profits’ were clearly the way to go.

Figure 17.3: The two coalitions: share of world market capitalization

Note: Series denote monthly data shown as 12-month moving averages.

Source: Datastream (series codes: TOTMKWD for world total, OILINWD for integrated oil; AERSPWD for defence; TECNOWD for technology).

But that was the peak. By the mid-1980s the situation started to change on several fronts. First, many developing countries, having shifted from import substitution to export-led growth, were now reclassified as ‘emerging markets’ open to foreign investors. Second, ‘high-technology’ was firing up both investor’s hype and the stock market, giving mergers and acquisition repeated shots of adrenalin. And third, neoliberalism, having undermined the previous statist ideology, now opened the door for massive privatization and capital decontrols. Put together, these developments marked the dawn of a new breadth regime.

The Weapondollar–Petrodollar Coalition started to decline, and by the early 1990s, with the Cold War over and the world having been declared a ‘global village’, it disintegrated. Signs of its demise were clear: international hostilities were actively curtailed, with the number of major conflicts falling from 36 in 1989 to 25 in 1997; military budgets the world over came under the axe, dropping by over one third in ‘real’ terms from their peak in the late 1980s; the price of oil fell absolutely and relative to other prices, reaching a low of $11 per barrel in 1999, compared with over $30 in the early 1980s ($96 in 2007 prices); and world inflation dropped to less than 5 per cent in 1999, down from over 30 per cent at the beginning of the decade.305

The main challenge to the Weapondollar–Petrodollar Coalition came from a new ‘Technodollar–Mergerdollar Alliance’, a group based on civilian high-tech and corporate takeovers and backed by Third-Way governments led by the likes of Bill Clinton and Tony Blair. Instead of ‘war profits’, nationalism and conflict, the new alliance marshalled the rhetoric of ‘peace dividends’ and free investment in an ‘open world’. Capital controls gave way to deregulation, protectionism to privatization, and bloody wars to peace deals. And indeed, by end of 2000, the Technodollar–Mergerdollar Alliance seemed victorious. As Figure 17.3 illustrates, its share of global market capitalization soared to 20 per cent, while that of the oil and armament companies sank to a meagre 4 per cent.306

Unrepeatable since time immemorial?

The retreat of breadth

During the 1990s, many experts, impressed by the new breadth euphoria, announced the arrival of a ‘new economy’ based on high-tech ‘knowledge’, ‘information’ and ‘communication’. This new economy, they promised, would deliver not only uninterrupted growth, but also low inflation, making the anomaly of stagflation a relic of history. Other observers with an eye to culture and politics went even further, arguing that liberal capitalism had won the last battle of ideology and that history was finally coming to an end. But the prognosis proved a bit hasty.

These projections hinged crucially on the promise of surging productivity. And yet, productivity growth data from the 1990s — assuming for argument’s sake that ‘productivity’ indeed can be measured — hardly seem exceptional by historical standards. In the United States, the presumed epicentre of the ‘high-tech revolution’, these data pale in comparison to the record of the ‘low-tech’ 1950s and 1960s. Moreover, past productivity gains have often failed to stop inflation, so it isn’t entirely clear why the experts expected them to succeed this time around. And, indeed, reports of the death of stagflation proved a bit premature.

The rapid breadth expansion, particularly in the emerging markets of Asia, created a massive build-up of excess capacity and loosened the grip of business sabotage. Green-field investment in the 1990s grew in leaps and bounds — much faster than world consumption and with disastrous consequences for profit margins. The implications for differential accumulation were not lost on absentee investors, who began liquidating their holdings in peripheral regions where earnings growth fell short of the world average (Nitzan 1997; 1998a). The first victim was the Mexican peso circa 1994, followed in 1997 by the Thai baht and the rest of the Asian currencies. From there the centrifugal forces of excessive external breadth spread devaluation throughout the developing world, striking most countries, from Russia and Brazil to South Africa and Argentina.

The emerging markets crisis spelled trouble for the core markets of North America and Europe. During the 1990s, developing countries absorbed some of the elevated hype from the core, and in so doing provided a defence line for ‘blue chip’ companies listed in the world money centres. Eventually, though, this defence line collapsed. In 2000, fear struck the core financial markets. Led by the collapsing NASDAQ, they went into a tailspin and in the process pulled the rug from under a two-decade surge in merger activity. Next, the global political economy, perhaps for the first time since the Great Depression, fell into a synchronized recession involving all major countries. And finally, after a decade of ‘peace dividends’, attacks on the World Trade Center and the Pentagon, followed by the invasion of Afghanistan and Iraq and the re-intensification of the Israeli–Palestinian conflict, rekindled the ghost of violence and ‘war profits’.

And so the tables again turned. As illustrated in Figure 17.3, by the early 2000s the Weapondollar–Petrodollar Coalition once more was on the ascent while the Technodollar–Mergerdollar Coalition went into a free fall.

Was the world running out of breadth? Were these developments the mark of a new depth phase? Or maybe they were soon-to-be-forgotten ripples on the tidal wave of globalization and amalgamation?

The boundaries of differential accumulation

In 1999, we presented a paper at the International Studies Association Meetings. The key question of the paper was stated in the title: ‘Will the Global Merger Boom End in Global Stagflation?’ (Nitzan 1999). And the answer was positive: based on our differential-accumulation framework, we argued that worldwide mergers and their neoliberal underpinnings were about to peak, and that conflict and stagflation were ready for a comeback.307

A decade later, such projections may seem trivial. The ‘global village’ is defunct; ‘No-Logo’ analysts have retreated, overshadowed by the pundits of terror and war; the headlines that previously announced prosperity and merger suddenly talk of stagnation and inflation; and the experts assure us that they have been predicting all of this all along.

But the truth is that, back in 1999, none of this was in the cards. Few in our audience understood the question we asked and even less so the answer we gave. Caught in the postmodern fashion of deconstruction, conditioned by the double separation of economics from politics and the real from the nominal, and indifferent to the speculative quantification of qualitative processes, they found our argument bizarre and our projections off the wall.

Our presentation, though, didn’t really try to ‘predict’ the future — at least not in the technical sense advocated by Karl Popper (1963). Instead, we attempted to delineate the limits of differential accumulation and to understand the boundaries they impose. And that is what we have done — with further analyses and details — in the present volume.

To reiterate, differential accumulation is a qualitative creordering of capitalist power that is speculatively quantified through the algorithm of capitalization. It is a conflictual process and is therefore open-ended. It doesn’t have to happen. If dominant capital increases its power, the rate of differential accumulation will be positive. But if this power stays the same or decreases, differential accumulation will be zero or negative, respectively. This is the general theoretical setting.

Now, using this framework we demonstrated: (1) that differential accumulation has proceeded more or less uninterruptedly for the past half-century and possibly longer; (2) that, historically, this accumulation occurred primarily though amalgamation and stagflation; and (3) that these two power regimes have grown increasingly counter-cyclical.

This theoretical–empirical framework enabled us to make our 1999 projection. As Figure 17.1 shows, by the late 1990s amalgamation was reaching historical highs while stagflation was approaching historical lows. The situation seemed ripe for reversion. There was no structural reason to expect differential accumulation to collapse, and since its two regimes were at historical extremes, it seemed safe to expect mergers to recede and stagflation to resurface. And that is exactly what happened in the decade since this projection was made.

Out of bounds

But correct projections do not mean that the social future is somehow foreseeable, let alone predetermined. The capitalist nomos is a creature of society, articulated and imposed by the ruling class on those who are ruled. No matter how ‘deterministic’ it may seem, this nomos is never ironclad. Created by humans, it can be changed — and indeed replaced — by humans. In the language of Gabriel García Márquez, it is ‘unrepeatable and therefore unpredictable since time immemorial’.

As long as dominant capital continues to rule, and as long as the logic of that rule remains unchanged, we can expect differential accumulation to oscillate between breadth through merger and depth via stagflation. Furthermore, since the breadth potential eventually is self-exhausting and since dominant capital is already in the final, global envelope, it seems reasonable to expect future stagflation cycles to become more frequent and deeper.

But, then, there is no certainty that dominant capital will continue to rule in the same way — or that it will continue to rule at all.

Over the past century, capitalists have managed to impose the belief that their regime is natural and therefore unalterable. They have constructed a power architecture that is more sophisticated, encompassing and supple than anything the world has ever seen. And they have successfully concealed this state of capital by erecting an anti-scientific front that fractures the consciousness and dresses up the power institutions of capitalism as if they were mere technical aspects of a narrow ‘economic narrative’.

This edifice of power and deceit hinges on the normal rate of return and the ability of dominant capital to beat it. As long as ‘business-as-usual’ sabotage and dissonance keep capitalists convinced that profit is normal and the growth of capitalization natural, and as long as dominant capitalists are able to exceed the normal and increase their power, the state of capital holds steady and its patterns remain ‘deterministic’.

But this ‘determinism’ is not an external law of nature or a historical law of motion. Instead, it is merely the ‘determinism’ of the capitalist rulers. The patterns of this ‘determinism’ reflect the consensus of those who dominate society. They show the conviction of the rulers that they are in command — and that those whom they command cannot resist. This conviction, though, is never certain. Confronted with sufficient opposition, whether explicit or implicit, it can crumble. And when it does crumble, the result is to shatter the ‘determinism’ of the rulers, the patterns of their differential accumulation and, possibly, the entire state of capital that defines their rule.

Postscript, January 2009

The research for this book was completed in early 2008. Since then, the capitalist world has been rattled by what many consider to be the deepest crisis since the Great Depression. The global shakeup has brought one aspect of our framework into sharp focus: it has shown that differential accumulation is by no means predetermined, and that it can fail.

The open-ended nature of the process is demonstrated most vividly by the increasing threat of deflation. As we have seen, over the past half-century, the capitalist creorder has been shaped by the differential accumulation of dominant capital, whose growing power is fuelled by the inversely oscillating regimes of breadth and depth. Although the two regimes differ markedly, both depend on rising prices: breadth through merger requires relatively low inflation, while depth through stagflation depends on high — and rising — inflation. This requirement was fulfilled in the post-war era, the longest period of uninterrupted inflation in human history (Figure 16.1).

But the inflationary backdrop also points to the limits of capitalist power. As noted in the introductory and concluding chapters, power is confidence in obedience: it represents the certainty of the rulers in the submissiveness of the ruled. In modern capitalism, this certainty is manifested in the ability of capitalists to control and systematize the upward movement of prices. And it is this ability — along with its associated confidence in obedience — that is totally lost during deflation. When prices start falling and the architecture of power begins to disintegrate, the rulers’ confidence fizzles and history suddenly seems open-ended.

And indeed, challenges to capitalist power often emerge when they are least expected. That was the case in 1929 — and again in 2000. By the beginning of the third millennium, dominant capital seemed unassailable. Using mergers and acquisitions, it had penetrated and transformed most developing countries into ‘emerging markets’; it had integrated former communist regimes into the logic of capitalization; and in the core countries it had imposed its own private ‘regulation’ while undermining public institutions of welfare and government. With the exception of small enclaves such as Cuba, Myanmar and North Korea, it had managed to subjugate and incorporate the entire world population into its all-encompassing nomos.

It was exactly at that high point, when the experts celebrated the end of history and the global village, that deflation suddenly struck. Mergers receded in the early 2000s — yet inflation, instead of rising, fell precipitously. This was no laughing matter. If disinflation turned into outright deflation, dominant capital would be bound to suffer differential decumulation. And that was just for starters. Deflation threatened to bring down the entire chain of debt obligations, whose size relative to GDP was much larger than it had been on the eve of the Great Depression. Had prices started to fall and debt to deflate, the spiral could quickly have become unstoppable.

The initial response was denial. Deflation simply was too dire to contemplate:

‘Ignore the Ghost of Deflation’, recommends Financial Times columnist Samuel Britton. ‘Apart from Japan’, he observed, ‘the world has not seen deflation for 70 years’ (as if the world’s second largest economy can be treated as an anomaly, and ‘70 years’ as a magic threshold beyond which deflation can never return). ‘Deflation is an overblown worry’, declares James Grant, editor of Grant’s Interest Rate Observer. ‘Believe in Ghosts, Goblins, Wizards and Witches if you will’, concurs financial expert Adrian Douglas, ‘but don’t believe in deflation occurring any time soon’. There is little to worry about, says Fed Chairman Alan Greenspan: ‘The United States is nowhere close to sliding into a pernicious deflation’. Of course, denying the problem does not solve it. And, so, for those who remain fearful, the experts promise that whatever the risk, it could easily be defused. ‘The good news’, announces former member of the Federal Reserve Board, Angell Wayne, ‘is that monetary policy never runs out of power’. ‘There’s a much exaggerated concern about deflation’, laments Nobel Laureate Milton Friedman. ‘It’s not a serious prospect. Inflation is still a much more serious problem than deflation. Today’s Federal Reserve is not going to repeat the mistakes of the Federal Reserve of the 1930s. The cure for deflation is very simple. Print money’. The same assumption underlies the soothing speech by Fed Governor Ben Bernanke, given in 2002 to the National Economist Club. In his address, properly titled ‘Deflation: Making Sure “It” Doesn’t Happen Here’, Bernanke explained that ‘Deflation is always reversible under a fiat money system’. ‘The U.S. government’, he assured his audience, ‘has a technology called the printing press that allows it to produce as many U.S. dollars as it wishes at essentially no cost’.

(Quoted from various sources in Bichler and Nitzan 2004b: 294–296)

But denial and promises didn’t work, so the experts called for action: ‘The Federal Reserve has won its long war against inflation’, wrote Chief Economist of Goldman Sachs Bill Dudley and Managing Director of Pimco Paul McCulley. ‘But to ensure an enduring legacy, Mr Greenspan now needs to solve a different problem: inflation is too low, rather than too high. . . . The inflation rate should be high enough to allow the economy to take a shock without falling into deflation’ (Dudley and McCulley 2003).

And Greenspan was more than ready to comply. He quickly reduced interest rates to levels not seen since the 1960s — and equally quickly realized he was pushing on a string. ‘In recent months, inflation has dropped to very low levels’, he complained to the Joint Economic Committee of the Congress. ‘Indeed, we have reached a point at which, in the judgment of the Federal Open Market Committee, the probability of an unwelcome substantial fall in inflation over the next few quarters, though minor, exceeds that of a pickup in inflation’ (Greenspan 2003). This was probably the first time since the 1930s that the Fed had pronounced lower inflation unwelcome.

In the end, though, it was the brinkmanship of the Weapondollar–Petrodollar Coalition that saved the day. The coalition managed to put the Bush clan back in the White House, inflame the Middle East, raise the price of oil and provide the necessary spark for inflation. That spark, though, merely helped delay the day of reckoning.

By 2007, storm clouds had started to gather again, and by early 2008 all hell had broken loose. Assets markets have gone into a free fall, followed by crashing commodity prices, collapsing employment and production, and broad inflation indices that are rapidly approaching zero. The threat of deflation, having been ridiculed by Nobel Laureates and dismissed by Central Bankers, is back with a bang.

Given the gravity of the situation, governments the world over have suspended their commitment to ‘free markets’ and ‘sound finance’ in favour of massive bailout packages for dominant capital, large fiscal stimuli, unprecedented injections of ‘liquidity’ and other policy rituals. In addition, there has been some increase in televised violence — from the erupting conflicts of the Middle East, to riots in Thailand, Greece and Korea, to promises of simmering discontent in Russia and China.

So far, though, policy and conflict have done little to lessen the deflation scare. Even the U.S. Federal Reserve Board sounds unnerved. Having reduced its interest rates to practically nil, it is now contemplating pleading directly with the public. According to this plan, the Fed will announce a positive ‘inflation target’; this announcement will then cheer up the depressed public and lift its inflationary expectations; and the inflation monster, having been invited in so politely, will rear up its beautiful head and give the Fed what it wants most: prices that go up (U.S. Federal Reserve Board 2008; Guha 2009).

These nervous calls to the omens suggest that capitalism again faces a historical crossroads. Renewed inflation will restore differential accumulation for dominant capital, initially through depth and perhaps later through breadth. But if the ruling classes are grabbed by panic and the power architecture disintegrates into deflation, the effect could be deeply transformative.

And that wouldn’t be the first time. During the 1930s, falling prices shook the capitalist world and eventually led to its complete creordering. Back then, the transformation ended up strengthening the state of capital. The imposition of capitalization on almost every aspect of social life, the ascent of dominant capital and the growing synchronization of breadth and depth helped create the most powerful mega-machine the world has ever known.

But the transformative outcome of deflation was not predetermined then, and it isn’t predetermined now. If prices start to fall in earnest, dominant capital might be seriously weakened — perhaps to the point of losing control over its very mode of power and the mega-machine that sustains it. Whether it can continue to rule, though, and in what way, remains an open-ended question. The answer to this question depends not only on what dominant capital does and how it does it, but also on the creativity, ability and courage of those who resist it in the hope of creordering an alternative, humane future.

Over the past century, the 30-year moving correlation between the stagflation and amalgamation indices in Figure 17.1 (with the latter index expressed as a natural log and measured as a deviation from its time trend) tightened almost to the fullest: it changed from a positive 0.06 in 1927 (virtually no correlation) to a negative 0.95 in 2007 (a nearly perfect inverse correlation).↩

The term itself is due to Michal Kalecki, who looked at the process from a class perspective. In his article ‘Political Aspects of Full Employment’ (1943b), he argued that liberal governments know how to achieve full employment and defuse the business cycle — but are unable to do so politically. Torn between their need to maintain their popular legitimacy on the one hand and to protect the capitalist class on the other, their policies often end up contributing to the business cycle rather than alleviating it.↩

Note again the bifurcated experience of the 1930s: as we mentioned in Chapter 12, most of the depression occurred in concentrated sectors, where production and employment fell by up to 80 per cent and where prices dropped very little or even rose. In the context of the times, this pattern was clearly stagflationary.↩

The growth and inflation figures in this and the next paragraph are computed from International Financial Statistics through Global Insight (series codes: L64@C110 for the consumer price index; and L66&I@C110 for industrial production).↩

For a more detailed examination of the Middle East and differential accumulation, see Nitzan and Bichler (1995), Bichler and Nitzan (1996), Nitzan and Bichler (2002: Ch. 5), Bichler and Nitzan (2004b) and Nitzan and Bichler (2006b).↩

The chart itself is meant merely to highlight the importance of conflict; the actual pattern of the conflict of course is far more complex and involves much more than arms exports.↩

The data for military exports here are based on the value of deliveries; if instead we were to display military contracts (which lead deliveries roughly by three years), the correlation would have been even tighter.↩

During the early 1990s, GDP growth in East Asia averaged 9 per cent, compared with less than 3 per cent in the industrialized countries. During that period, transnational corporations based in the United States saw their net profit from ‘emerging markets’ rise to 20 per cent of the total, up from 10 per cent in 1980s (Nitzan 1996b).↩

Although government deficits declined to around 1 per cent of world GDP in the late 1990s, down from their all time high of over 5 per cent in the early 1980s, government expenditures haven’t fallen. They have risen from 14 per cent of GDP in the 1960s to 17 per cent in the 1980s, and remained more or less at that level since then (computed from World Bank Online). The privatization of such services — including transportation, water, infrastructure, education and security — typically takes the form of giving/selling them to dominant capital, which in turn contributes to differential accumulation in a manner similar to green-field investment.↩

For an exploration of these ‘internal’ politics of differential accumulation, see Nitzan and Bichler (2002), Bichler and Nitzan (2004b) and Nitzan and Bichler (2006b).↩

For a detailed history and analysis of this coalition, see Nitzan and Bichler (1995) and Bichler and Nitzan (1996).↩

Calculated from International Financial Statistics through Global Insight (series code: L64@C001 for CPI in the industrialized countries; L76AA&Z@C001 for the price of crude oil; and L64@C111 for the US CPI); the Stockholm International Peace Research Institute (Annual); and the U.S. Arms Control and Disarmament Agency (Annual).↩

For a similar comparison based on the distribution of global net profit, see Nitzan and Bichler (2006b: p. 80, Figure 12).↩

For subsequent articulations of this argument, see for example Nitzan (2001), Faux (2002) and Nitzan and Bichler (2003) and Bichler and Nitzan (2004a).↩